closed end loan disclosures

The revisions also banned several advertising practices deemed deceptive or misleading. For closed end dwelling-secured loans subject to RESPA does it appear early disclosures.

2

1 The amount or percentage of any downpayment.

. In a closed-end consumer credit transaction secured by a first lien on real property or a dwelling other than a reverse mortgage subject to 102633 for which an escrow account was established in connection with the transaction and will be cancelled the creditor or servicer shall disclose the information specified in paragraph e2 of this section in accordance with the form. For a closed-end transaction secured by real property or a dwelling other than a transaction that is subject to 102619e and the creditor shall disclose a statement that there is no guarantee the consumer can refinance the transaction to. A good faith estimate of expected closing costs such as loan origination fee loan discount appraisal fee assumption fee interest on per-day basis.

If a closed-end consumer credit transaction is secured by real property or a cooperative unit and is not a reverse mortgage the creditor discloses a projected payments table in accordance with 102637c and 102638c as required by 102619e and f. These disclosures must be used for mortgage loans for which the creditor or mortgage broker. Or 4 The amount of any finance charge.

Regulation Z Closed End Disclosure Content for Mortgage Loans. Disclosures for mortgage loans secured a members primary residence that are subject to RESPA. For a closed-end transaction secured by real property or a dwelling other than a transaction that is subject to 102619e and the creditor shall disclose a statement that there is no guarantee the consumer can refinance the transaction to.

Thus for most closed-end mortgages including construction-only loans and loans secured by vacant land or by 25 or more acres not covered by RESPA the credit union must provide the. Regulation Z Closed End Disclosure Content for Mortgage Loans. Format of Regulation Z.

Only applies to loans for the purpose of purchasing or initial construction of and secured by the consumers principal dwelling. The regulation was also revised to reflect the 1995 Truth in Lending amendments that dealt primarily with tolerances for loans secured by real estate and limitations on lenders liability for disclosure errors for these types of loans. If the actual fee charged exceeds the disclosed amount by more than 10 percent the lender will have to cover that cost at closing.

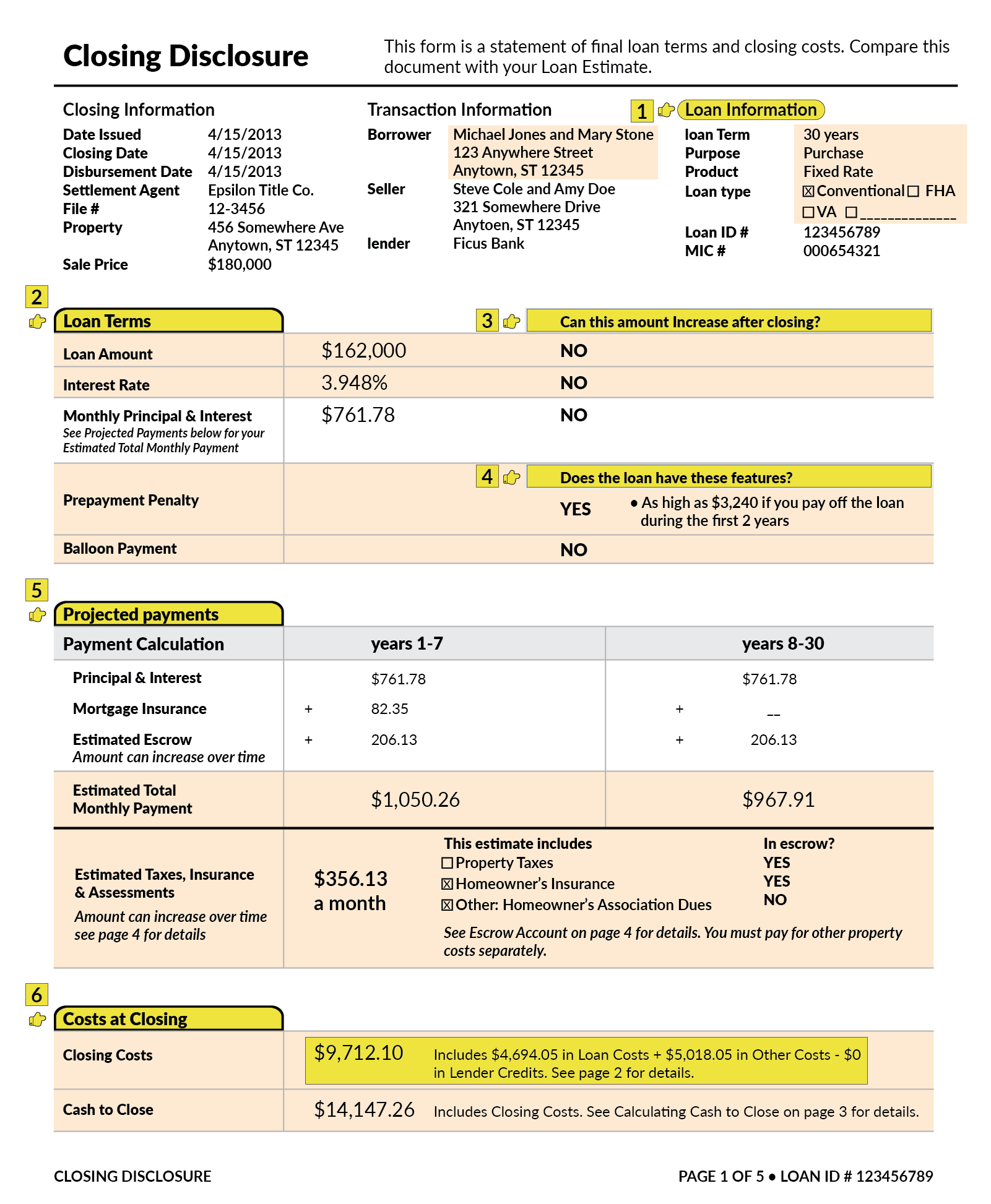

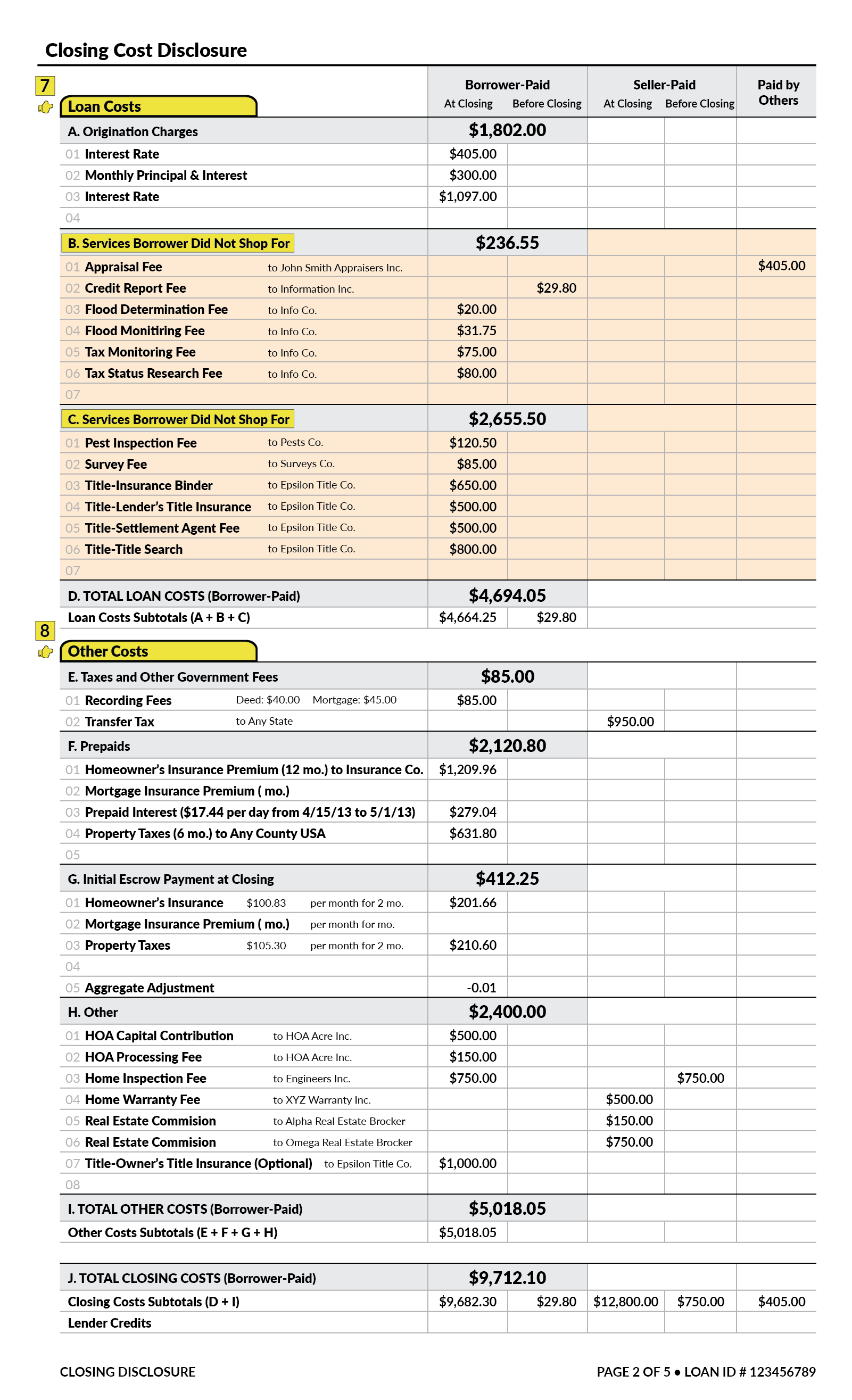

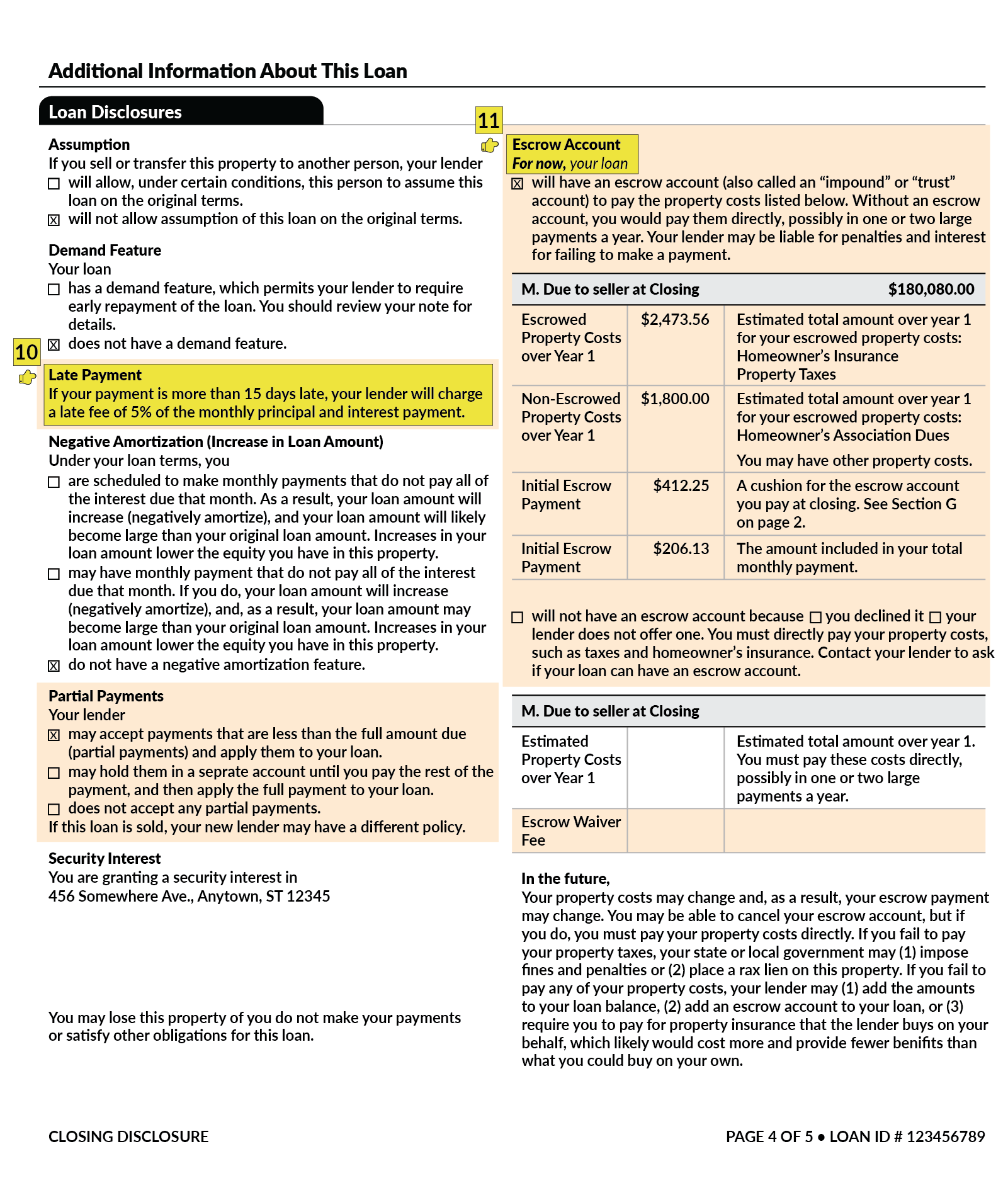

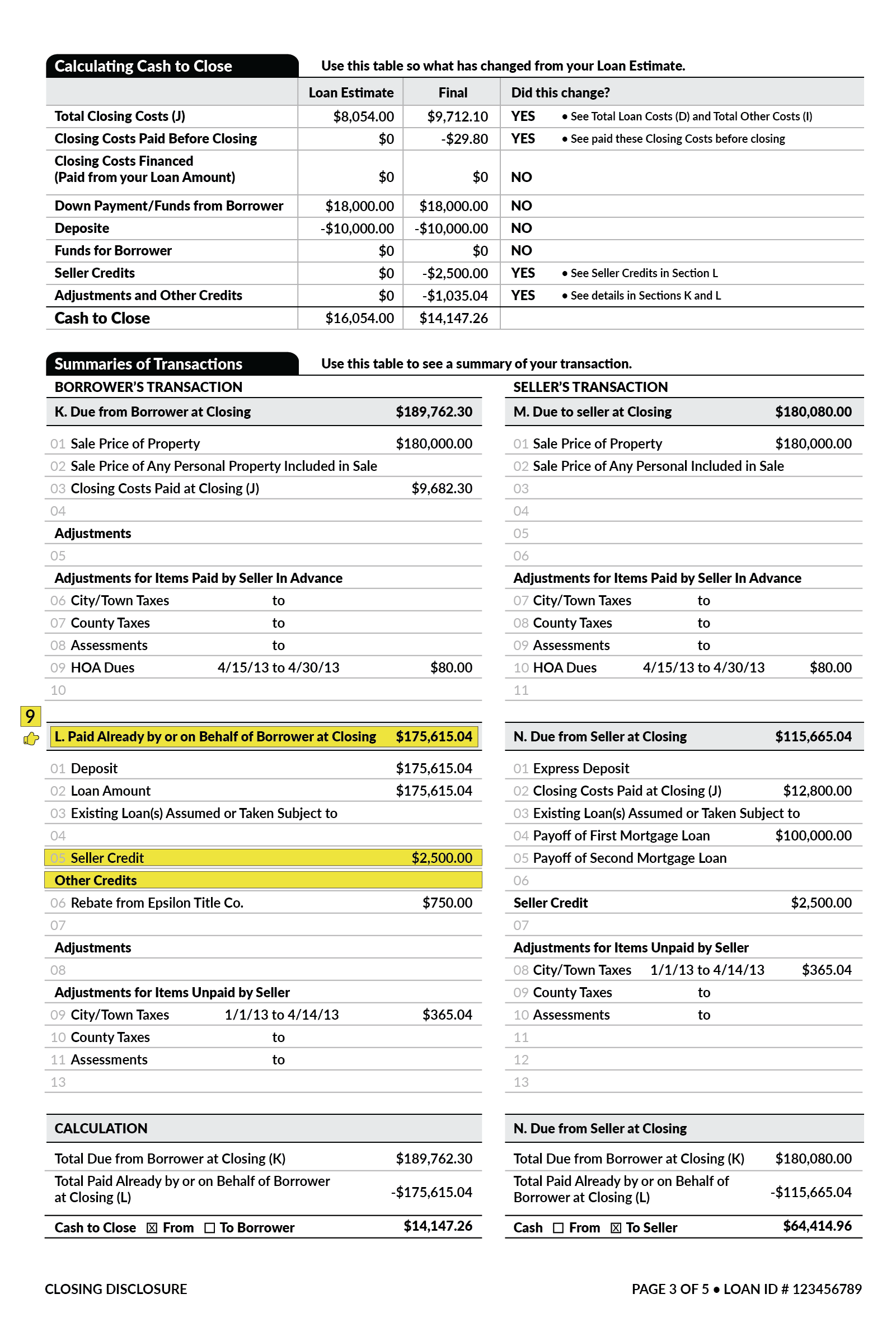

If disclosures are delayed until conversion and the closed-end transaction has a variable-rate feature disclosures should be based on the rate in effect at the time of conversion. This requirement is only applicable to first. Use our Closing Disclosure Explainer to review and understand the details within your disclosure before closing on your mortgage loan.

Trigger terms when advertising a closed-end loan include. 2801 VIA FORTUNA SUITE 600 AUSTIN TX 78746 Page 1 of 2800 569-3665 WWWSMSLPCOM. Closed-end subprime loans secured by a consumers principal dwelling.

3 The amount of any payment. The Loan Estimate and Closing Disclosure must be used for most closed-end consumer mortgages secured by real property or a cooperative unit. Requires certain disclosures be made to the member before consummation of a closed-end home equity loan.

Except for home equity plans subject to 102640 in which the agreement provides for a. The revisions also applied new protections to mortgage loans secured by a dwelling regardless of loan price and required the delivery of early disclosures for more types of transactions. The Loan Estimate must be in.

Closed-end consumer credit transactions secured by real property or a cooperative unit other than a reverse mortgage subject to 102633 opens new window are subject to the disclosure timing and other requirements under the TILA-RESPA Integrated Disclosure rule TRID. Unfortunately noif during the loan term a HELOC is converted from open-end credit to closed-end credit that would trigger closed-end credit requirements including the TRID disclosures as set out here. The disclosure packet will also have the truth in.

Converting open-end to closed-end credit. Stating No downpayment does not trigger additional disclosures. These disclosures must be used for mortgage loans for which the creditor or mortgage broker receives an application on or after August 1 2015.

Requirements under the TILA-RESPA Integrated Disclosure rule TRID. If consummation of the closed-end transaction occurs at the same time as the consumer enters into the open-end agreement the closed-end credit disclosures may be given at the time of conversion. Of the disclosures you list here would be the status in a closed-end home equity loan.

2 The number of payments or period of repayment. Most closed -end consumer mortgage loans. Only applies to purchase-money loans subject to RESPA.

The Loan Estimate is provided within three business days from application and the Closing Disclosure is provided to consumers three business days before loan consummation. For closed-end credit transactions secured by real property Reg Z 102619 requires Credit Unions to provide members with good-faith estimates of credit costs and transaction terms on a document called the Loan Estimate. Thus for most closed-end mortgages including construction-only loans and loans secured by vacant.

Converting open-end to closed-end credit. Higher-cost closed-end mortgage loans and included new disclosure requirements for reverse mortgage transactions. Good Faith Estimate of Settlement Costs.

Regulation Z Closed End Disclosure Content for Mortgage Loans. The Loan Estimate is provided within three business days from application and the Closing Disclosure is provided to consumers three business days before loan consummation. The Federal Reserve has published several rules implementing certain provisions of the Mortgage Disclosure Improvement Act MDIA.

Some lenders may provide you with an initial loan worksheet which can be any type of document explaining your estimated rates terms and payments based on initial information youve provided. Depends on lien position. Home equity lines of credit reverse mortgages and mortgages secured by a mobile home or by a dwelling other than a cooperative unit that is not attached to real property ie.

Home Equity Oak Tree Business Home Equity Equity Mortgage Loans

About The Tila Respa Integrated Closing Disclosure Nfm Lending Payroll Records Payroll Software

U Slides Legislative Legal Updates Mortgage Loan Mortgage Help

How To Comply With The Closing Disclosure S Three Day Rule Alta Blog

Understanding Finance Charges For Closed End Credit

Fraud Prevention Tip Talk To Someone Before You Give Up Your Money Or Personal Information Talk To Someone You Trus You Gave Up Credit Union Company Culture

What Is A Closing Disclosure Lendingtree

Home Buying Process Infographic Home Buying Process Home Buying Home Buying Tips

What Is A Closing Disclosure Lendingtree

What Is A Closing Disclosure Lendingtree

Closed End Home Equity Application Credit Union Form Http Www Oaktreebiz Com Products Services Closed End Home Equi Home Equity Home Equity Loan Loan Account

Businessman Standing On A Stack Of Guide Books Looking Forward Through A Telescope Https Cumanagement Com A Effective Leadership Leadership Roles Leadership

Home Oak Tree Business Identity Fraud Credit Union Business Systems

What Do Those Investment Terms Really Mean Forum Credit Union Financial Tips Investing Budgeting Tips

What Is A Closing Disclosure Lendingtree

Have You Heard The News Credit Union Lending Is On The Rise According To The Latest Federal Reserve Report Home Equity Credit Union Marketing Line Of Credit

Truth In Lending Act Tila Consumer Rights Protections

/alta-sellers-closing-statement-26837264d4044785a5d0409dae83a510.jpg)

Closing Statement Definition

Infographic The Loan Process Simplified Mortgage Marketing Online Mortgage Mortgage Infographic